![]()

![]()

![]()

![]()

What Is the Widow’s Penalty and Why Can Taxes Rise After a Spouse Dies?

Share:

Table of Contents

The widow’s penalty is described as a tax problem that can hit after a spouse dies: filing status shifts from married filing jointly to single, and the single brackets are less favorable. A surviving spouse can reach higher brackets sooner while trying to maintain income.

Key Takeaways

- The widow’s penalty is described as a tax squeeze created when filing status shifts from married filing jointly to single, compressing bracket room.

- In the year of death, married filing jointly can still apply for the full tax year, creating a one-year planning window.

- When a spouse dies, one of the two Social Security payments goes away, and the survivor generally assumes the higher benefit.

- Replacing lost income with traditional IRA withdrawals is described as ordinary income and can create a compounding tax effect.

- Roth IRA withdrawals are described as tax-free and not increasing taxable income, supporting survivor income replacement.

- Life insurance death benefits are described as tax-free and not counted toward provisional income for Social Security taxation.

How Much Do Tax Brackets Change When Filing Shifts From Married to Single?

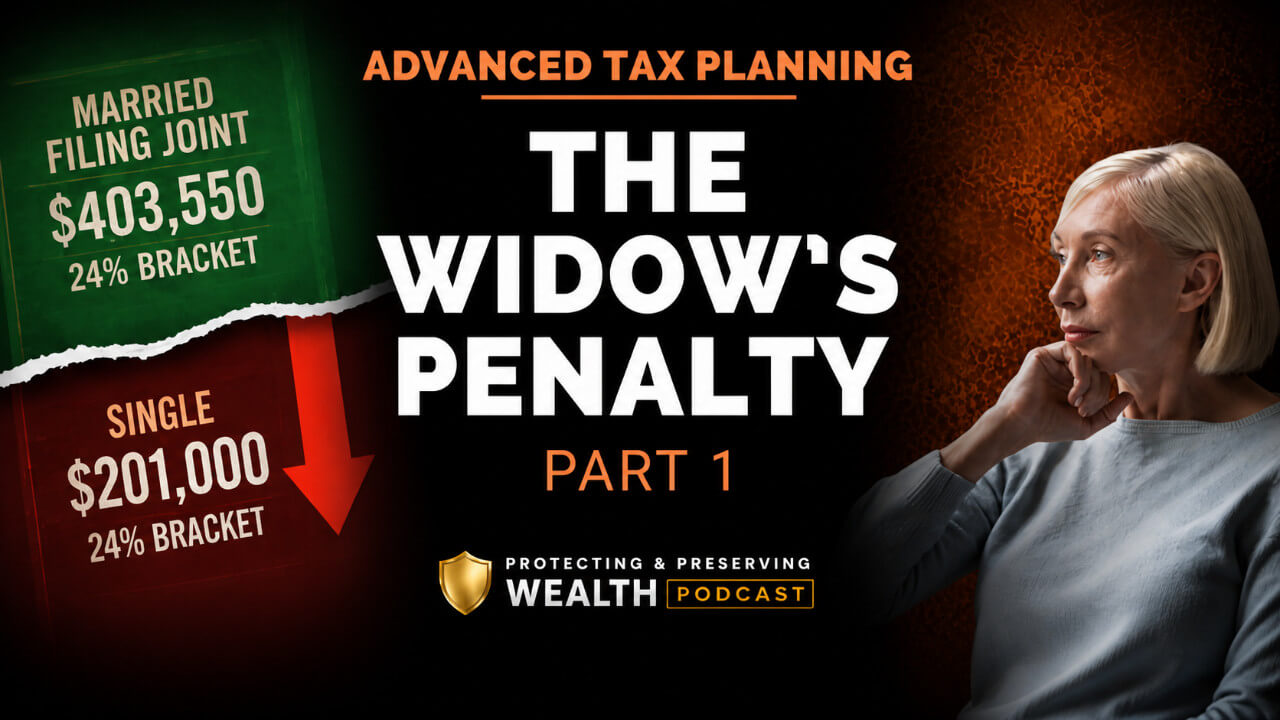

In 2026, the 24% bracket for married filing jointly is described as allowing income up to $403,550. The 24% bracket for a single filer is described as maxing out at $201,000—“literally less than half” in the example given.

Who Is Most Likely to Face This, and How Long Can the Survivor Need the Plan to Work?

Cerulli and Associates (2024) is cited: 95% of spousal heirs are expected to be women, and over $54 trillion is expected to pass to surviving spouses before children inherit. CDC life expectancy data is referenced: widows could live 4 to 12 years past the death of a spouse.

Why Are Many Widows Unprepared for the Financial Responsibilities After a Death?

A 2024 survey is cited: about 56% of married women defer long-term financial decisions, and 98% of widows regret not being more involved earlier. A stated planning goal is for both spouses to know what is owned, why it is owned, what each asset is supposed to do, and to be able to answer: “Am I going to be okay?”

What Tax Planning Window Exists in the Year of Death?

In the year a spouse dies, married filing jointly can still be used for that entire tax year. That creates a larger bracket that can be used for planning purposes discussed.

What Planning Moves Are Mentioned for That One-Year Window?

- Roth conversions are called out as a primary use of the larger bracket in that year.

- “Stacking deductions” is discussed, including using a donor-advised fund and donating highly appreciated assets (examples given: real estate, stocks, artwork) to create a larger deduction in that year.

What Happens to Social Security When One Spouse Dies?

When the higher-earning spouse dies in the scenario discussed, one Social Security payment goes away, and the surviving spouse assumes the higher payment. The household is described as losing one of the two checks, creating an income gap that often needs replacement.

Why Can Replacing a Lost Social Security Check Increase Taxes?

Replacement income is described as often coming from additional withdrawals from a tax-deferred retirement account, taxed as ordinary income. Social Security is described as potentially taxed “up to 85%,” while an IRA distribution is described as “100% taxable.”

A compounding risk is described: more withdrawals create more taxable income, which creates more taxes, which can require more withdrawals.

How Does a Roth IRA “Tax-Free Bucket” Change the Income Replacement Math?

Withdrawals from a Roth IRA are described as tax-free and not increasing taxable income. Having a tax-free bucket available after a spouse dies is described as “huge” for replacing lost Social Security income or lost pension income without increasing the taxable situation.

How much of an IRA to convert to Roth.

Are Life Insurance Death Benefits Taxable, and Do They Affect Social Security Taxation?

Life insurance death benefits are described as tax-free to beneficiaries (no federal taxes and no state taxes stated). Those proceeds are also described as not counting toward provisional income for Social Security taxation.

What Can a Chronic Care Rider Do for Long-Term Care Planning and Independence?

Chronic care riders are described as allowing acceleration of a life insurance death benefit to pay for long-term care expenses if qualifying criteria are met. Qualifying is referenced as trouble with two of the six activities of daily living, with examples including eating, transferring, toileting, and managing medications.

A specific benefit description is given: a chronic care rider is described as providing 25% of the death benefit for care if qualifying criteria are met, and described as indemnity (not reimbursement).

What Households Match the Fact Pattern Discussed?

- Married filing jointly today, with a likely future shift to single filing after the first death.

- Two Social Security payments today and the loss of one payment after a death.

- Tax-deferred retirement accounts being used for income replacement.

- Roth conversions being considered while favorable married brackets exist.

- Life insurance planning and chronic care rider planning as tools for survivor support and long-term care risk.

- Estate planning basics.

- Services (tax planning / Roth conversion planning / LIRP planning).

Summary

The widow’s penalty is described as a combined squeeze: filing status shifts from married filing jointly to single with materially tighter brackets, one Social Security payment goes away, and income replacement often comes from taxable IRA withdrawals that can compound taxes over time. Planning opportunities described include using the year-of-death married filing jointly window for Roth conversions and potentially stacking deductions, building a tax-free Roth bucket for survivor income flexibility, and using life insurance and chronic care riders to support independence and long-term care planning.

Additional Educational References

- Social Security Administration: Survivors Benefits (publication).

- IRS: Life insurance proceeds generally not includable in gross income.

- IRS: Roth IRAs overview.

- IRS: Instructions for Form 8606 (includes Roth conversion reporting context).

- IRS: Donor-advised funds overview.

For more information about anything related to your finances, contact Bruce Hosler and the team at Hosler Wealth Management. Contact Our Team: https://www.hoslerwm.com/contact-us/

Call the Prescott office at (928) 778-7666 or our Scottsdale office at (480) 994-7342.

To view all Protecting and Preserving Wealth Podcast episodes: https://www.hoslerwm.com/protectingwealthpodcast/

Limitation of Liability Disclosures: https://www.hoslerwm.com/disclosures/

Copyright © 2026 Hosler Wealth Management | All Rights Reserved. #ProtectingWealthPodcast #ProtectingandPreservingWealthPodcast #HoslerWealthManagement #BruceHosler

Produced by JAG Podcast Productions – https://www.jagpodcastproductions.com.

Host

Bruce Hosler is the founder and principal of Hosler Wealth Management which has offices in Prescott and Scottsdale, Arizona. As an Enrolled Agent, CERTIFIED FINANCIAL PLANNER® professional, and Certified Private Wealth Advisor (CPWA®), Bruce brings a multifaceted approach to advanced financial and tax planning. He is recognized as a prominent financial professional with over 29 years of experience and a eight-time consecutive *Forbes Best-In-State Wealth Advisor in Arizona. Bruce recently authored the book MOVING TO TAX-FREE™ Strategies For Creating Tax-Free Retirement Income And Tax-Free Lifetime Legacy Income For Your Children. www.movingtotaxfree.com.

In the Protecting & Preserving Wealth podcast, Bruce and his guests discuss current financial topics and provide timely answers for our listeners.

If you have a topic of interest, please let us know by emailing info@hoslerwm.com. We welcome your suggestions.

2018-2025 Forbes Best In State Wealth Advisors, created by SHOOK Research. Presented in April 2025 based on data gathered from June 2023 to June 2024. Not indicative of advisor’s future performance. Your experience may vary. For more information please visit.

Guest Profiles

Alex Koury is a CERTIFIED FINANCIAL PLANNER® professional, a CERTIFIED PRIVATE WEALTH ADVISOR (CPWA®), and holds a Certified Exit Planning Advisor (CEPA®). Working out of our Scottsdale office, he has been in the financial services industry for over 15 years. He holds Series 7, 9, 10 & 66 securities registrations– and is a Registered Representative with Mutual Group.

Jason Hosler holds Series 7 and 66 FINRA securities registrations. He brings a technological edge to our firm and helps many of our clients stay current in the fast-moving age of the internet.

Bruce Hosler, Jason Hosler, and Alex Koury were collectively recognized as 2025 Forbes Best-In-State Wealth Management Teams, reflecting their collaborative approach to comprehensive wealth, retirement, and advanced tax planning. This recognition is a fantastic milestone for us, and it inspires us to continue delivering outstanding service to our valued clients every day.

2025 Forbes Best-In-State Wealth Management Teams, created by SHOOK Research. Presented in Jan 2025 based on data as of March 2024. 11,674 Management Teams were considered, approximately 5,300 teams were recognized. Not indicative of advisor’s future performance. Your experience may vary. For more information, please visit.

Transcript

Protecting and Preserving Wealth Episode 84 – The Widow’s Penalty

Speakers: Bruce Hosler, Jason Hosler, Alex Koury, & Jon Gay

[Music playing]

Jon Gay (00:05):

Welcome back to Protecting & Preserving Wealth, I’m Jon Gay. I’m joined as always by Bruce Hosler, Jason Hosler, and Alex Koury of Hosler Wealth Management. Gentlemen, always good to be with you.

Bruce Hosler (00:14):

Good to be with you, Jon. Thank you.

Jason Hosler (00:15):

Good to see you, Jon.

Alex Koury (0:17):

Always, Jon. Good to see you.

Jon Gay (00:19):

So, we’re going to do a two-part series. Today’s the first in a two-part series that we’re calling The Widow’s Penalty. And this is a really interesting topic. Bruce, let’s set the stage with the pretty easy question. What is the widow’s penalty?

Bruce Hosler (00:32):

So, Jon, that’s a great question in the industry, and there’s all kinds of ramifications about it. But the one that comes to mind most importantly has to do with taxes. And so, while we’re a married couple, we get to file our tax returns as married filing joint. And the limits on what the tax rates are, are much more favorable. So, let me give you an example.

In 2026, in the 24% tax bracket (which is my favorite tax bracket for married couples that are trying to do Roth conversions), they can have income up to $403,550 and remain in the 24% tax bracket. So, if their regular living income is $100,000 or $200,000, they can probably convert a couple of hundred thousand a year into a Roth conversion. No big deal.

But the widow’s penalty is … and it’s a widow’s penalty because (and we’re going to talk about the statistics here in a second) when the old guy dies, she’s left with all of the income and a much lower tax bracket.

So, the 24% tax bracket for a single person is maxed out at $201,000. So, it’s literally less than half, and she could be in a much higher tax bracket when that happens. So, that’s the widow’s penalty. Let’s talk about some of the statistics.

A lot of clients are planning their estate planning, and they’re thinking about leaving money to their children. But the first thing we want to address here is you really might be leaving it to your spouse. And are you leaving enough, and are they going to be okay? And how do you do that?

Now, according to Cerulli and Associates in 2024, 95% of spousal heirs will be women, and there will be over 54 trillion (that’s with a T) that will pass to surviving spouses, mostly women, before children will inherit any money.

Alex, what is the average number of years that widows will outlive their husbands when we look at the statistics?

Alex Koury (02:43):

Great question. Likely, a lot longer now that they don’t have this nag looking over their shoulders every two seconds.

[Laughter]

But realistically, widows could live 4 to 12 years past the death of their spouse. That’s a long, long time that they need to be prepared to take on the financial responsibilities of the family wealth.

Bruce Hosler (03:04):

And Alex, that’s from the CDC. That’s life expectancy data. So, ladies, this message is for you and your husbands that love you. 4 to 12 years on your own is what they’re expecting just from real statistics.

Jon Gay (03:20):

And again, it sounds like we’re singling out wives who outlive their husbands, but you just said the numbers a moment ago, Bruce. Statistically, most of the time, the wife does outlive the husband.

Bruce Hosler (03:32):

Yes.

Jason Hosler (03:32):

And Jon, these widows are often unprepared for life after the death of a spouse. Oftentimes, they’ve deferred long-term financial decisions to their husband. The numbers that we have from a 2024 survey is about 56% of married women defer those long-term financial decisions, and 98% of widows regret not being more involved in their family finances earlier.

So, how we can help when both spouses are living is by having the conversation about the widow’s penalty. What are we going to do for you after your husband most likely predeceases you? How do we handle the estate planning in that situation? What can we do while you’re both still alive to prepare for that eventuality?

Jon Gay (04:22):

I want to jump in for a second because I have to give my wife credit here. I’m the exception to the rule because my wife works in corporate finance. So, she actually runs the finances for our house. But she always is saying to me, “Hey, let me show you all these numbers so you know what’s going on.”

And I am very often, “Oh, you got it handled. I’m going to go watch the game or something.” But it’s a really good point that both partners in a relationship should really be aware of where everything is and why everything is the way it is.

Bruce Hosler (04:51):

I want to address this for a second. We want them to know what they own, why they own it, what it’s supposed to do for them, that particular asset. And finally, the most important question that they ask is, “Am I going to be okay?”

We want the financial plan for that. Now, I want to give husbands and wives … in your case, you’re the husband, but in other spouses, it may be the wife. But in either case, what happens in a marriage is you have a division of labor.

He takes care of the trash, she cleans up the dishes, and that’s the way they divide. And maybe he vacuums and she’s decorating. Whatever the division of labor is – he fills the cars with gas, she never has to fill gas, but she pays the credit card bills, however it may be.

And sometimes, there’s one (in your case, it’s your wife) that does the finances, and you’re bringing in the bread in the front door, and she’s paying the bills or whatever. But this division of labor (just like Jason talked about), we want the ladies to be involved and come to the meetings and become educated on these topics if they don’t normally have an interest in that.

And many of them don’t because their husband wants to control it and he’s interested, and that happens. I want to address now the widow’s penalty, how that happens.

So, let’s say the old guy passes away and dies.

Jon Gay (06:19):

Or the young guy.

Bruce Hosler (06:20):

Or the young guy. We’re going to deal with both of those. So, the first consequence is she can no longer file married filing joint. So, right now, we’re in early 2026, and let’s just say … well, I did. We just had a friend at church; he just passed away unexpectedly.

What’s the opportunity for her before the end of the year that she could take advantage of that married filing joint?

Jason Hosler (06:49):

So, in the year that a spouse dies, you can still file married filing joint for that entire tax year. And you have a larger bracket that you can utilize for a couple of different purposes. The first one that comes to mind is obviously doing a Roth conversion and filling up that bracket.

There are other planning opportunities that can arise out of having that married filing joint. Is there an opportunity to stack some deductions as well in that year?

Bruce Hosler (07:21):

When you say “stack deductions,” what is the primary way to stack deductions? What can you do to take deductions that you wouldn’t normally? Where do you make that contribution or donation?

Jason Hosler (07:33):

If you have donations that you can pull forward from future years that you’d be making, you could make a donation to a donor-advised fund. And it’s kind of-

Bruce Hosler (07:42):

Of highly appreciated assets, right? Whether it’s real estate or stocks or other artwork, you can donate that and get your big deduction in that one year, and then raise your income up and offset those two, right?

Jason Hosler (07:56):

Yeah. Optional medical is often something that we see for deductions as well. But really, when you’re in that situation where you know that in the next year, you’re going to have lower single filing tax rates, I think that the Roth conversion is a really big one to utilize in that year.

Because if you do have significant funds still in your traditional IRA, getting that moved over at the more advantage tax rate to the tax-free bucket so you can utilize that in your higher tax years later on, that just makes a lot of sense.

Bruce Hosler (08:32):

So, the next thing on the widow’s penalty that I want to talk about, Alex, is about social security and how social security works. And let’s just say that the husband was the breadwinner most of the years and he had higher wages, she worked some, she had some wages. They’re both receiving social security.

What happens when he dies to his social security and what happens to hers, and how does this apply to the widow’s penalty?

Alex Koury (08:59):

Yeah, great question there. So, what happens is when the husband dies in this situation, who is earning more money than the surviving spouse, the wife in this situation loses her benefit that she was receiving for her social security.

But she also assumes the higher-paying social security payment that was the husband’s. So, she does get a step up in the actual guarantee of social security benefits she gets, but there’s also a loss of income because one of the social security payments does have to go away.

Bruce Hosler (09:30):

So, she’s losing as a household, paying the household bills. Folks, the widow’s penalty is she’s losing one of the two social securities. So, her income is going down by half or whatever that social security amount is.

That’s one aspect of the widow’s penalty that we want to talk about. So, that income and that loss of income, now has to be made up. So, where, Jason, do a lot of people, if they have tax-deferred money, where is she going to make up that money from?

Jason Hosler (10:06):

She’s going to her retirement account. She’s going to start taking additional withdrawals, which are going to be taxed as ordinary income.

Bruce Hosler (10:15):

And it’s going to increase her taxable income because that social security (even if they were high enough income folks to have their social security taxed) is only taxed up to 85%. If she has to replace the same amount of income from an IRA distribution, it’s 100% taxable.

So, she has just had her income tax and taxable income go higher, trying to maintain the same amount of income, and she has to now pay more taxes. Oh, now, she has to pay more taxes, Alex, where is she going to go to get the extra money to pay the taxes?

Alex Koury (10:56):

Well, if you’re taking it from, again, a tax-deferred account or an IRA, then the monies that come from the IRA are more than likely to pay that tax as well. And again, that’s a distribution. That’s also additional income that is also taxable.

So, you can see in your mind how this can compound and snowball into a bigger problem because now, there’s more income, more taxes that could whittle away over time quicker than someone would really realize or think about.

Bruce Hosler (11:22):

Now, Jason, you were talking earlier about the Roth IRA, what if they have listened to us and they have been converting their IRAs? Maybe they’re not 100% converted, but she has a big pile of money in a Roth IRA, and she still has a taxable IRA.

If she needs that additional income to make up for the loss of social security, does that increase her income to take it from that Roth?

Jason Hosler (11:46):

The Roth IRA being tax-free isn’t going to increase her taxable income. So, having that bucket, the tax-free bucket available after a spouse dies, is huge because you can make up for lost social security income or lost pension income.

A lot of our clients have pensions with maybe a 50% or a 75% survivor benefit because they wanted a higher payout. Well, that loss of income being made up from the tax-free bucket isn’t going to increase your taxable situation.

So, you can see in a situation where you have a surviving spouse that having that bucket ready makes it much easier to replace the income. So, getting ahead on your Roth conversions while you’re both alive, you have the favorable tax brackets can really make a difference in income replacement when you have the surviving spouse.

Bruce Hosler (12:38):

This is great information, guys. Now, I just want to finish up this particular one. We’re going to talk about naming a spouse beneficiary in part two and all the ramifications of that. But I want to talk about life insurance for a minute.

Now, let’s just say we talk about LIRPs (life insurance retirement plans), and we’re going to talk about two different policies. He had a policy on him, and she has her own life insurance policy. Now, when he dies, does her policy pay off?

Does not.

But when he dies, the proceeds from that life insurance policy, are those taxable, Alex?

Alex Koury (13:17):

The answer is no. The death benefit you receive from your life insurance policy is a tax-free benefit to your beneficiaries.

Bruce Hosler (13:28):

So, no federal taxes, no state taxes. Does that payment make her social security taxable?

Alex Koury (13:34):

No, it does not count towards your provisional income, which is also great as well. So, again, when you think about just holistic planning of strategizing in all the buckets that you can use at your disposal, again, tax-free income counts way more than leaving tax-deferred or other taxable assets like a brokerage account potentially.

Bruce Hosler (13:52):

So, Jason, she still has her life insurance policy, and assuming that it has a chronic care rider on it, she is now alone. She doesn’t want to live with the kids; she doesn’t want to be a burden to the kids. She doesn’t want to be dependent on the kids. She wants to be independent.

What does that life insurance policy, chronic care rider, give her that she wouldn’t have otherwise without that policy?

Jason Hosler (14:22):

So, those chronic care riders are a benefit from the life insurance policy that allows you to accelerate and pay out the death benefit of the life insurance policy towards long-term care expenses. So, if you qualify under the rules, two of the six activities of daily living – and we’ve talked about those before.

Eating, transferring, toileting, managing your medications – so, if you have trouble with two of those and you need that care, that death benefit can be accelerated and help you pay for that care. So, it’s another way that these tools can be used to help in your overall planning and making sure that the surviving spouse is taken care of after the first is deceased.

Bruce Hosler (15:14):

I just want our listeners to imagine their mother, or their wife, or their sister is now a widow, and she has in her hip pocket her life insurance policy with that chronic care rider that’s going to give her 25% of the death benefit of her life insurance policy to have any care that she needs. It’s not reimbursement, so that policy will just pay out if she qualifies (it’s indemnity). How does she feel?

I want you to imagine she knows that if she needs to go into a nursing home, or let’s say she doesn’t want to go into a nursing home, she wants to stay home and have somebody come in and care for her, the independence and the security that having that knowledge gives her, and the security of having that ability to pay for that care and having money set aside specifically for that, that doesn’t affect the inheritance for the children – it affects her ability to care for herself. This is a great gift for that little, sweet widow.

And I just want to paint that picture for our listeners to let them know that this type of planning is very, very important for the well-being and the mental security that it provides to our clients and to the people that have that.

Jason Hosler (16:44):

And once again, that’s why it’s really important that even if you are the spouse who’s not managing money, that you come to at least a certain number of the meetings that you have with your advisor and your planning team, so you know what’s the expectation of what’s going to happen. What are we doing to prepare for these eventualities?

If you are a married couple that is over 65, you have two-thirds of a chance that you’re going to need long-term care. So, either you’re choosing to pay for that yourself, or you’re choosing to transfer that risk to an insurance company. One way or another, you’re most likely going to need to pay for at least some long-term care.

So, those considerations, the considerations on beneficiaries at the death of the first spouse. And a lot of times, we also have mixed marriages and mixed families. All of those considerations need to be recognized and planned for, for families before the death of the first spouse.

Jon Gay (17:49):

I think that’s really a great place to leave it. If one of our listeners or viewers wants to come talk to you and the team at Hosler Wealth Management about estate planning, anything related to their financial future, what are the best ways to reach you?

Bruce Hosler (17:59):

We’d love them to reach us at hoslerwm.com, or they can call us on the phone in Prescott, Jason?

Jason Hosler (18:05):

In Prescott, give us a call at (928) 778-7666.

Bruce Hosler (18:10):

And it’s Scottsdale, Alex, how can they get to you?

Alex Koury (18:12):

Give me a call at (480) 994 7342.

Jon Gay (18:17):

The Widow’s Penalty, we’re going to pick up with part two next time. We’ll talk to you guys then.

Jason Hosler (18:22):

We’ll see you then, Jon.

Bruce Hosler (18:23):

Thank you, Jon.

Alex Koury (18:24):

Bye, Jon.

[Music playing]

Disclosure: (12:56):

Investment advisory services are offered through Mutual Advisors LLC, DBA Hosler Wealth Management, a SEC registered investment advisor. Securities are offered through Mutual Securities, Inc., a member FINRA/SIPC. Mutual Advisors, LLC and Mutual Securities, Inc. (collectively Mutual Group) are affiliated companies.

Forward-looking commentary should not be misconstrued as investment or financial advice. The advisor associated with this podcast is not monitored for comments, and any comments should be given directly to the office at the contact information specified.

Any tax advice contained in this communication, including any attachments, is not intended or written to be used and cannot be used for the purpose of 1) avoiding federal or state tax penalties; 2) promoting marketing or recommending to another party any transaction or matter addressed herein; and 3) tax preparation and accounting services are offered independently through Hosler Wealth Management Tax Services.

Any tax advice provided by tax professionals under Hosler Wealth Management Tax Services is separate and unrelated to any advisory or security services offered through Mutual Group. The accuracy, completeness, and timeliness of the information contained in this podcast cannot be guaranteed. Mutual Group does not provide tax or legal advice. You should consult a legal or tax professional regarding your individual situation.

Accordingly, Hosler Wealth Management does not warranty, guarantee or make any representations or assume any liability with regard to financial results based on the use of the information in this podcast.

Be The First To Know About New Podcast Episodes!

"*" indicates required fields